LHCSA Budgeted Projections Statement Instructions

- Instructions are also available in Portable Document Format (PDF)

Required for:

Licensed Home Care Services Agencies (LHCSA)

Contents

Introduction

New Home Care agencies, or existing agencies looking to expand into new counties or offer new services and require a budgeted Medicaid Fee-for-service (FFS) reimbursement rate, are required to submit the Budgeted Projections Statement. This information will be used by the Department of Health (DOH) to calculate a budgeted rate. The instructions contained within apply to agencies that operate one or more of the following entities:

- Licensed Home Care Services Agency (LHCSA)

An agency is defined as an organization that operates one or more LHCSA . Agencies that operate one or more of these facilities must complete certain parts of the Budgeted Projections Statement for each of these entities.

An entity is defined as a LHCSA. An entity may be operated as part of a larger agency or may be free-standing.

Agencies that require a budgeted rate for a Certified Home Health Agency (CHHA) should contact DOH for guidance and instructions by emailing CHHA-Rates@health.ny.gov.

The Budgeted Projections Statement will require the completion of the general information schedules (1 and 2), and rate setting schedules (3, 4, 5, and 7). If your agency previously completed a standard Home Care Cost Report, you may notice that the budgeted projections statement is more streamlined and does not include all schedules included in the standard cost report. Please note that this is intentionally done to reduce reporting requirements for budgeted requests. Some of the schedules in the Budgeted Projections Statement will require information at the agency level, while other schedules require information at the entity level. The instructions explicitly state which schedules of the Budgeted Projections Statement require agency-level information and which schedules require entity-level detail (LHCSA) to be reported. A note is included at the beginning of each section to indicate if agency or entity-level information is required.

A The letter "A" indicates a schedule requires agency -level information to be reported.

E The letter "E" indicates a schedule requires entity -level information to be reported.

Reporting Guidance

Since Medicaid reimbursement rates for LHCSAs are calculated by county, entity-level information will need to be broken out separately on schedules where this detail is required. For the purposes of this projections statement, LHCSA entities are required to be separated by county. For example, if a LHCSA provides services in two counties, then that agency is said to have two entities for the purposes of the Budgeted Projections Statement submissions. In addition, some agencies may have office locations that service multiple counties. An entity should not be identified based on the physical office locations, but rather the county served. A unique LHCSA entity is associated with one county.

Please note that all Budgeted Projections Statement schedules will be completed in the Home Care Tool. The Tool is a web-based platform that will create a customized view of only the schedules of the projections statement required to be completed for your agency and the entities operated by the agency. Based on the information you enter in the "Budgeted Reporting Hierarchy" tab of the Tool, only the required schedules will be visible to complete in the "Budgeted Projections Statement" tab. Note that further details related to the Tool can be found in the "Completion of Web-based Tool" portion of the Budgeted Instructions tab.

The Budgeted Projections Statement instructions specify that a standard set of rules be followed to provide consistent data for comparison purposes. DOH reserves the right to reject the information submitted if the instructions are not properly followed.

Important Items to Note

- Allocation Methodology

Schedules 3 and 4 of the Budgeted Projections Statement require an allocation methodology be used to allocate total agency budgeted costs to the different entities and service types. DOH recommends using budgeted Operating Expenses as the basis to allocate budgeted data within the Budgeted Projections Statement. If a provider is unable to use this approach, they can explicitly document the allocation methodology they used (e.g., Hours of Service, Square Feet Occupied, Time Study). - Costs

Please note that you are required to report the budgeted costs for one calendar year when completing the Budgeted Projections Statement. In addition, the Budgeted Projections Statement must include all agency budgeted costs (regardless of payor source, i.e., Medicaid, Medicare, third-party insurance, or private pay). All budgeted costs should be recorded as positive values. The Tool will not allow negative values to be entered on Schedules 3 or 4.

The term "reimbursable" is used throughout the Budgeted Projections Statement instructions and the Tool to refer to services that are reimbursed by DOH through Medicaid Personal Care Programs. This reimbursement can be through Medicaid FFS, Managed Care/MLTC, or through a contract with NYC Human Resource Administration (HRA). If a cost or service type is "nonreimbursable," that means that the reimbursement from DOH flows through a program OTHER than Personal Care Programs.

Note: Please refer to Appendix A for the Personal Care Rate Codes. - Contracting Relationships

As part of the delivery of services, many agencies have contracting relationships with other agencies to perform direct care services. For example, there are instances where an agency will contract the delivery of services to another agency. If both agencies reported the costs of these services as reimbursable, this would result in double counting. As such, only the primary agency contracting the services should report them as reimbursable. If your agency previously completed a standard Home Care Cost Report, you may be familiar with the reporting of expenses paid to a subcontractor when your agency is acting as the primary contractor. Your agency may also be familiar with reporting costs incurred when your agency is acting as the subcontractor and providing services on behalf of the primary contractor. For the purposes of the budgeting process, it is only necessary to report expenses that your agency anticipates paying as the primary contractor. These costs can be the cost of direct employees or contracted staff. If a subcontractor relationship exists in the future where actual services are provided and payments are made, instructions will be available to clarify proper reporting in the regular Home Care Cost Report. If your agency anticipates having direct care contracting relationships, please follow these reporting instructions to report the estimated costs from the anticipated contracting relationship. Note that further instructions regarding contracting relationships are covered within the instructions for Schedule 3b of this document.

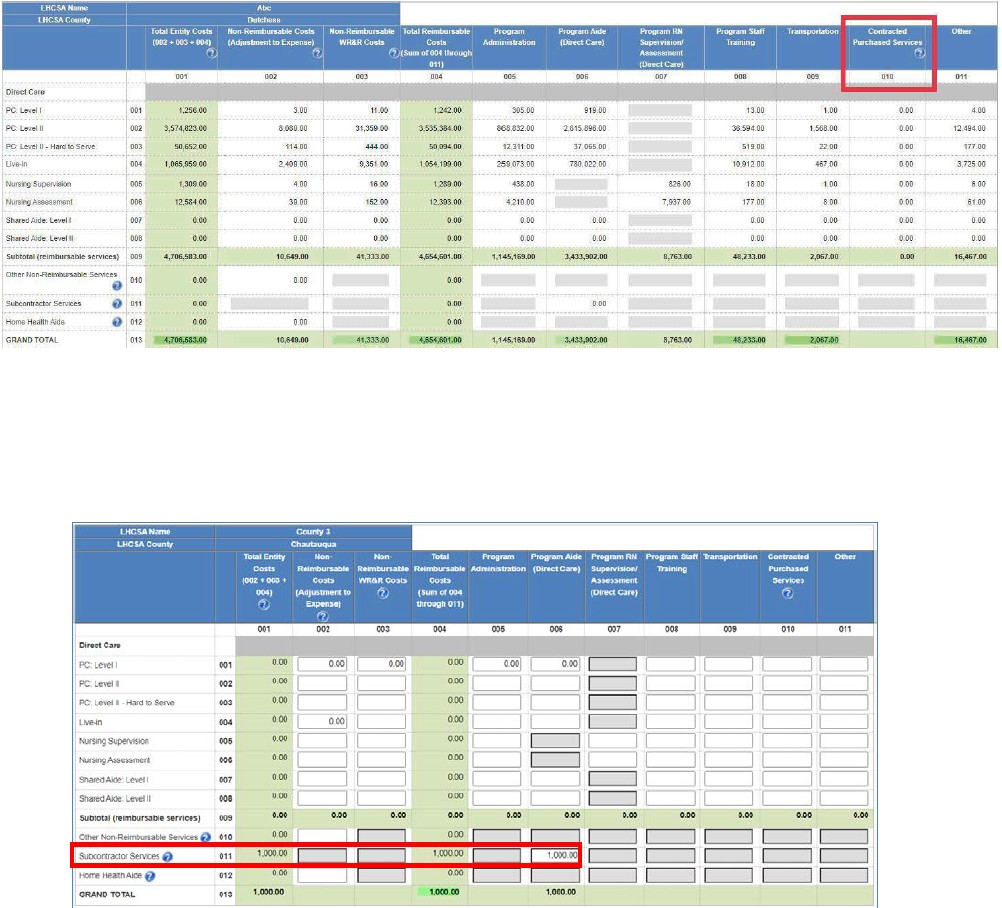

Agency purchasing a direct care service from another agency (primary contractor)

The agency contracting the direct care services should report the budgeted costs they expect to incur purchasing the service in the "Contracted Purchased Services" Column 010, within the applicable service type row on Schedule 3, as shown in the screenshot below. - Vendors

Agencies may use a vendor to assist with Budgeted Home Care Projections Statement preparation and submission. If an agency uses a vendor to support the projections statement, the agency is still responsible for accurate and timely submissions and responses to any inquiries. Please also note that an executive-level individual will need to sign off on the completeness and accuracy of the Budgeted Projections Statement data prior to submission (e.g., CEO or CFO). - Procedural Recommendations

- Agencies should develop internal Budgeted Projections Statement policies and procedures to help ensure that budgeted costs are reported properly. Documented policies and procedures will allow for consistent reporting in the event that new rate(s) are needed in the future to support a new program or location. The policy and procedures document should include projections statement preparation instructions that are specific to the agency, such as the sources of data that are necessary to complete the projections statement, how budgeted costs should be allocated on different schedules, and who is responsible for preparing and reviewing the report.

- In an effort to demonstrate segregation of duties during the projections statement submission process, agencies should have multiple individuals involved in the preparation, review, and submission of the projections statement.

- Automatic Tool Checks

- There are automatic checks in the Tool that will help providers identify potential errors in their Budgeted Projections Statement prior to submission. If a potential error is identified, then a warning message will appear when the agency attempts to mark the schedule as complete. The warning message will describe the potential error and provide helpful guidance on how the agency can correct the potential error. If there are several errors, then the agency will see a warning message for each error. Once the agency has corrected the potential error, the warning message will disappear.

- At the top of each projection statement schedule, there is a "click here to view validation warnings for this schedule and all submitted schedules" button. To identify potential errors that have not been corrected, the agency can select this button.

- In the Tool, there are several checks that are recommended, but not required. Agencies are not required to correct these prior to submission but are asked to provide an explanation if these are not corrected. To see these error(s), click the "click here to view validation warnings for this schedule and all submitted schedules" button. Agencies will be able to provide an explanation within this popup window.

- There are a few required checks that will prevent submission if these errors are not corrected as these are considered essential to the process. These checks are summarized below:

- Medicaid Management Information System (MMIS) ID numbers entered within the Budgeted Reporting Hierarchy must be 8 digits

- Federal Tax ID numbers entered within the Budgeted Reporting Hierarchy must be 9 digits.

- Entity tables are not blank on Schedules 3, 4, or 5

- Budgeted costs entered in Program Administration (Column 005) on Schedule 3

- Budgeted costs entered in Program Aide (Column 006) or Program RN Supervision/Assessment on Schedule 3

- Budgeted costs entered in Program Administration (Column 001) on Schedule 4

- Program Administration totals on Schedule 3 (Column 005) and Schedule 4 (Column 001) are equal at the agency and entity levels

- Service type rows for statistics reported on Schedule 5 match to the service type rows for the corresponding costs reported on Schedule 3

- Patient counts reported under each payor type on Schedule 5 have corresponding units of service for each service type within each payor type, and vice versa.

- Service statistics entered in "Dual-eligible" (Columns 010 to 013) for a specific service type row, were also entered into "Medicare" (Columns 004 to 006) or "Medicaid" (Columns 001 to 003) for that same service type, and that the Dual-Eligible amount is equal or lower than the sum of the Medicaid and Medicare columns.

Schedule 1: General Information - Agency

A Note: Schedule 1 contains agency-level information.

This General Information Schedule contains information on the agency level. The information that will appear on this schedule includes the following:

Agency Information

- Name of Agency: Enter the legal name of the organization.

- Alternative agency name or DBA (if applicable): Enter any DBAs ("doing business as") or alternative names the agency may be used for identification purposes.

- Federal Tax ID: Enter the Federal Tax ID of the organization.

- Agency Type: Select the agency type (Proprietary, Voluntary, or Public).

- Address: Enter the street address of the agency headquarters.

- City: Enter the name of the city where the agency headquarters is located.

- State: Enter the state where the agency headquarters is located.

- Zip: Enter the zip code for the agency headquarters.

Note: If your agency has previously completed and submitted a Home Care Cost Report within the web-based Tool under the same Federal Tax ID, your agency should complete this process using the same Tool Account that has already been set up for your agency. In this scenario, the information listed above will auto-populate. This will help to ensure that this information is the same and will not require re-entry. If your agency has questions about an existing Tool Account, please contact the following mailbox: us-advrisknyshc@kpmg.com.

Contact Person Information

The name of the person that can answer questions regarding the Budgeted Projections Statement submission. Include this person's first and last name, job title, telephone number, and email address (required fields).

Entity Types

Information should be entered in for the total quantity of unique LHCSA entities that will be operated by the agency. For example, if your agency expects to operate 2 LHCSA entities, "2" should be entered for the LHCSA line items. Please enter a value of "0" for FI entity types. Do not leave any of these fields blank.

Please note that this information for Schedule 1 will be entered in the "Budgeted Reporting Hierarchy" tab of the Home Care Tool. All information entered in this location will automatically populate in the "Budgeted Projections Statement" tab (location where the Budgeted Projection Statement schedules are to be completed).

Schedule 2: General Information - Entity

E Note: Schedule 2 contains entity-level information.

Note: Schedule 2 contains entity -level information.

This General Information Schedule contains information at the entity level and will populate the below information for each of the LHCSA entities operated by the agency. The number of tables that appear on this schedule will correlate with the total number of LHCSA entities that appear on Schedule 1. For example, having 2 LHCSA entities in Schedule 1 would result in two Schedule 2 tables appearing. These tables will populate automatically based on the information entered in the "Budgeted Reporting Hierarchy" tab of the Tool.

Information that will appear on this schedule (depending on entity type) includes the following:

Entity Information

- Name of Entity: Enter the legal name of the organization.

- Type: Select the entity type (Proprietary, Voluntary, or Public) from the drop-down menu.

- Address: Enter the street address of the entity headquarters.

- City: Enter the name of the city where the entity headquarters is located.

- State: Enter the state where the entity headquarters is located.

- Zip: Enter the zip code for the entity headquarters.

- County Served: Select the county where services are expected to be provided by this entity from the drop-down box.

- MMIS ID Number: Enter the MMIS ID Number of each LHCSA entity. Note : All Medicaid Management Information System ID numbers should be eight digits.

- License Number: Enter the License Number of any LHCSA entities.

- Direct Care Standard Hours Per Work Week: Enter your entity's standard work week for a direct care worker (e.g., 40 hours per week). This would be the standard hours for an individual and would not include items like overtime.

- Program Administration Standard Hours Per Week: Enter your entity's expected standard work week for an administrative worker (e.g., 37.5 hours per week). This would be the standard hours for an individual and would not include items like overtime.

- Reporting Period (From and To): Enter time period during the Budgeted Projections Statement year that the budgeted data will be reported for the entity.

Contact Person

The name of the person that can answer questions regarding the Budgeted Projections Statement submission. Include this person's first and last name, job title, telephone number, and email address (required fields).

Schedule 3b: Costs and Expenses

E Note: Schedule 3b requires entity-level information.

Schedule 3b requires the reporting of budgeted costs and expenses by service type for each LHCSA entity operated by the agency. Note that an agency is required to complete more than one of the following schedules if they expect to operate more than one of these entity types:

- Schedule 3b (for budgeted LHCSA costs and expenses) - A separate Schedule 3b table should be completed for each unique LHCSA entity.

Please follow the below instructions while completing Schedule 3b.

- — While supporting documentation is not required to be provided for the Budgeted Projections Statement, it will be required in future years when the agency submits the completed Home Care Cost Report. All supporting documentation will be uploaded to the Secure File Transfer Protocol (SFTP) site at the following link: https://kmft.us.kpmg.com/.

- — For your Budgeted Projections Statement submission, the costs are expected to be estimated as you have either not begun operations or have been in operation for less than a year. Examples of source documentation that agencies may be used to prepare the Budgeted Projections Statement Schedule 3 include:

- Operating Budget for full calendar year (Board approved, if available)

- Annualized Trial Balance

- Budgeted Financial Statements

- — Budgeted data should be entered in Columns 002 and 005 through 011 of Schedule 3. Columns 001 and 004 will be automatically calculated based on the information entered into Columns 002 and 005 through 011. No data should be entered into Column 003 (Nonreimbursable WR&R Costs) for the Budgeted Projections Statement.

- — All budgeted costs reported on Schedule 3b should be recorded as positive values (actual budgeted expenses). The Tool will not allow negative values to be entered on Schedules 3 or 4.

- — Budgeted costs must be allocated to the appropriate service type rows for the services offered or expected to be offered so that budgeted rates for each service type provided can be established.

- Each entity table is broken down into two sections: reimbursable services and nonreimbursable services. The "Subtotal (reimbursable services)" row will calculate the total of the reimbursable service type expenses only. The "Grand Total" row will calculate the sum of the reimbursable and c service type expenses.

- — A description of the costs that should be entered in each column of Schedule 3b is included below:

- Column 001: Total Entity Costs - Column 001 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 002 (Nonreimbursable Costs), Column 003 (Nonreimbursable WR&R costs - N/A for Budgeted Projections Statement) and Column 004 (Reimbursable Costs). The Total Entity Costs value should reconcile to the total budgeted expenses per the agency's operating budget, annualized trial balance, or budgeted financial statements for the full calendar year.

- Column 002: NonReimbursable Costs (Adjustment to Expenses) - Include in this column the estimated expenses that are considered nonreimbursable by DOH through Medicaid Personal Care Programs, which should not be included in 005 through 011. To be considered as reimbursable in determining reimbursement rates, budgeted costs shall be properly chargeable to necessary patient care. Reimbursable costs shall be determined by the application of the principles of reimbursement developed for determining expected payments under Title XVIII of the Federal Social Security Act (Medicare) program. Budgeted costs that are nonreimbursable in nature include, but are not limited to, the below list. When assessing whether a budgeted cost is reimbursable, note that reimbursable costs shall not include the following:

- Amounts in excess of reasonable or maximum title XVIII of the Federal Social Security Act (Medicare) costs or in excess of customary charges to the general public. This provision shall not apply to services furnished by public providers free of charge or at a nominal fee.

- Expenses or portions of expenses reported by individual entities which are determined by the commissioner not to be reasonably related to the efficient production of patient care services because of either the nature or the amount of the item.

- Costs not properly related to patient care or treatment which principally afford diversion, entertainment, or amusement to owners, operators, or employees of agencies or entities.

- Meal expenses and advertising costs for the purposes of attracting patients.

- The following taxes are not reimbursable:

- Federal and State Income taxes

- City taxes

- Sales taxes on purchases paid to NYS and the county

- NYS Health Facility Cash Assessment Program (HFCAP)/Cash Receipt Assessment tax

- Health Care Workers Bonus expenses which were funded through the NYS Health Care and Mental Hygiene Worker Bonus (HWB) Program.

- Any interest charged related to rate determination or penalty imposed by governmental agencies or courts, and the costs of policies obtained solely to insure against the imposition of such a penalty.

- Costs of contributions or other payments to political parties, candidates, or organizations and charities.

- The interest paid to a lender related through control where the approval of the Commissioner of Health has not been obtained (for costs incurred on or after January 1, 1992).

- Costs related to the provision of nonreimbursable services, meaning services that are reimbursed through a program other than Personal Care. Examples of nonreimbursable services for each entity type are summarized in the chart below:

Nonreimbursable service Applicable entity type Assisted Living Program (ALP) services LHCSA Private duty nursing services LHCSA Programs of All-Inclusive Care for the Elderly (PACE) services LHCSA Nursing Home Transition and Diversion (NHTD) services LHCSA Traumatic Brain Injury (TBI) services LHCSA Home Health Aide *LHCSA Out-of-state services LHCSA Non-home-care services LHCSA - *Includes subcontracting HHA services and direct HHA services contracted with MCO(s). Since reimbursement for these services is not received directly through Medicaid FFS, no Medicaid FFS rate will be provided for this service. Costs for HHA services to a LCHSA agency are deemed nonreimbursable for cost reporting purposes.

- — Costs related to the above nonreimbursable services should be reported in the "Other nonreimbursable services" row 010, within Column 002 (Nonreimbursable costs).

- — Nonreimbursable costs should be recorded as positive values. The portion of total costs that is nonreimbursable should be separated from the costs reported in Columns 005-011 and reported in Columns 002 and 003. The total reimbursable plus nonreimbursable costs should add up to the agency's total costs.

- Column 003: Nonreimbursable WR&R Costs : This column is not applicable to Budgeted Projections Statement. Data should not be entered in this column as WR&R revenue was not previously received.

- Column 004: Total Reimbursable Costs - Column 004 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 005 through Column 011. Below is a description of reimbursable budgeted costs that are to be used when completing Columns 005 through 011.

- Column 005: Program Administration - All Program Administration (Personnel and Non-Personnel) budgeted costs should be reported in Column 005 on Schedule 3. For a list of the Program Administration costs, please refer to the Schedule 4, Column 001 instructions on pages 18 through 21.

Further descriptions of each of the Program Administration expense categories are included in Appendix B.

Important notes:- — The Grand Total row of Column 005 (Program Administration) on Schedule 3 should equal the Grand Total row of Column 001 (Program Administration) on Schedule 4. The Program Administration budgeted costs are the same on Schedules 3 and 4 but are allocated in different ways. On Schedule 3, program administration budgeted costs are allocated across the different service type rows that the agency provides or expects to provide using an allocation methodology (see on page 4 of this document for a description of allocation methodology).

- — If any professional staff will split their time between administrative and direct care services, their personnel expenses (e.g., salary, benefit, and payroll tax expenses) should be allocated across the Program Administration (Columns 005) and Direct Care (Columns 006 and 007) columns based on the expected time they will work performing each type of service.

- Column 006: Program Aide (Direct Care) - Report budgeted expenditures related to the direct provision of care by program aides specific to LHCSAs . Information in this column should not include nursing supervision or nursing assessment expenditures. Examples of information to be reported in this column include the following:

- Direct care worker salary/compensation

- Direct care worker benefits & payroll taxes:

- FICA taxes (Social Security + Medicare)

- Life/Health Insurance

- Pension & Retirement

- Disability/Unemployment/Workers' Compensation

- Medical Supplies

- Other costs that can be directly attributable to the provision of care

- Column 007: Program RN Supervision/Assessment (Direct Care) - Budgeted costs reported in this column should include any direct care services provided and expected to be billed under procedure codes T2024 (Nursing Supervision) and T1001 (Nursing Assessment) for Managed Care and rate codes 2742 (Nursing Supervision) and 2787 (Nursing Assessment) for FFS. These budgeted costs should be reported in the appropriate Nursing Assessment and Nursing Supervision service type rows (005 and 006). Any direct care RN Supervision and Assessment budgeted costs related to the ongoing supervision, training, assessment of the aides not billable under procedure codes T2024 and T1001 and rate codes 2742 and 2787, should still be reported as direct care expenses within Column 007, but should be allocated among the billable service type rows that the supervision/assessment services relate to and reported in Column 007 for each applicable service on Schedule 3. Examples of information to be reported in this column include the following:

- Program RN Supervision/Assessment worker salary/compensation

- Program RN Supervision/Assessment worker benefits & payroll taxes:

- FICA taxes (Social Security + Medicare)

- Life/Health Insurance

- Pension & Retirement

- Disability/Unemployment/Workers' Compensation

- Other costs that can be directly attributable to the provision of care related to nursing supervision and nursing assessment.

- Column 008: Program Staff Training - Report any budgeted training costs. All Program Staff Training (Direct Care Personnel, Administrative Personnel, and Non- Personnel) costs should be reported in Column 008 on Schedule 3. Column 008 costs should be allocated to the appropriate service type rows on Schedule 3.

- Column 009: Transportation - Report budgeted transportation related costs for direct care workers, such as gas and mileage. Administrative transportation costs should not be reported here, but rather should be reported in Column 005 (Program Administration).

Note: Costs associated with paying direct care workers to travel (travel time wages) should not be reported here, but rather should be reported in Column 006 (Program Aide [Direct Care]) or Column 007 (RN Supervision/Assessment) along with other direct care wages. - Column 010: Contracted Purchased Services - Report budgeted expenditures associated with direct care services provided by agencies or individuals who are not employees of the agency/entity. The primary agency contracting the direct care service should report the budgeted costs they expect to incur purchasing the service in Column 010 Contracted Purchased Services, within the appropriate service type row on Schedule 3.

- Column 011: Other Costs - Report budgeted expenditures associated with items that cannot be appropriately included in the other columns in Schedule 3b. Items entered in this column may require an explanation and description to indicate the nature of the budgeted cost. A reconciliation may also be required to explain the budgeted costs reported here.

For more information related to the Direct Care line items, please reference the Appendices for information relating to billing codes for direct care services.

Schedule 4b: General Service Cost Centers

E Note: Schedules 4b require entity-level information.

Schedule 4b requires the reporting of budgeted general service cost centers for each LHCSA entity operated by the agency. Note that an agency is required to complete more than one of the following schedules if they expect to operate more than one of these entity types:

- Schedule 4b (for budgeted LHCSA general service costs) - A separate Schedule 4b table should be completed for each unique LHCSA entity.

Please follow the below instructions while completing Schedule 4b.

- — While supporting documentation is not required to be provided for the Budgeted Projections Statement, it will be required in future years when the agency submits the completed Home Care Cost Report. All supporting documentation will be uploaded to the Secure File Transfer Protocol (SFTP) site at the following link: https://kmft.us.kpmg.com/.

- — For your Budgeted Projections Statement submission, the costs are expected to be estimated as you have either not begun operations or have been in operation for less than a year. Examples of source documentation that agencies may be used to prepare the Budgeted Projections Statement Schedule 4 include:

- Operating Budget for full calendar year (Board approved, if available)

- Annualized Trial Balance

- Budgeted Financial Statements

- Square footage report

- Mileage log

- — Please note that Schedule 4 should contain budgeted administrative personnel costs and non-personnel costs. Direct care worker wages and benefits should not appear on Schedule 4. The Tool will not allow negative values to be entered on Schedules 3 or 4.

- — A description of the costs that should be entered in each column of Schedule 4b is included below:

- Column 001: Program Administration - All Program Administration (administrative personnel and non-personnel) budgeted costs should be reported in Column 001 on Schedule 4, within the appropriate cost center row. Program Administration costs should be reported in the following general service cost center rows on Schedule 4:

- — Row 001: Criminal Background Check & Fingerprinting: Expenditures related to conducting background check and fingerprinting of potential employees prior to hiring.

- — Row 002: Capital Related - Building & Fixtures: In this category, report the acquisition cost, freight, delivery, and installation charges to maintain or improve fixed assets, such as buildings. Non-capitalized items included within expenses on Financial Statements and Trial balances would be reported in this column.

- — Row 003: Capital Related - Movable Equipment: In this category, report the acquisition cost, freight, delivery, and installation charges of minor equipment and furnishings, such as typewriters, adding machines, chairs, and tables. Noncapitalized items included within expenses on Financial Statements and Trial balances would be reported in this column.

- — Row 004: Plant Operations & Maintenance: In this category, report all costs of operations, maintenance, and repairs expensed during the year.

- — Row 005: Rent - Building, furnishings, vehicles: In this category, report all rental costs, including installation charges, if any, of leased building, vehicles, equipment, or furnishings. Include in this line all rental charges paid by the lessee specified in the lease agreement.

- — Row 006: Interest - Property: Interest expense on bank loans, bonds, mortgages, or similar instruments is reimbursable if such expense was incurred to finance the purchase of fixed assets, major equipment, furnishings, or vehicles utilized to provide patient care services.

- — Row 007: Depreciation - Plant, equipment & furnishings, vehicles: An allowance for capitalized buildings, vehicles, equipment, and furnishings based on accepted accounting principles using the original acquisition cost or donated value if title is held by the provider entity. The straight-line method should be used in conformity with the useful lives stated in "American Hospital Association Estimated Useful Lives of Depreciable Hospital Assets," latest edition.

- — Row 008: Transportation: Expenditures for travel expenses incurred for administrative purposes only. These expenditures should include items such as flights, reimbursable travel meals, gas, and mileage.

- — Note: Travel time wages should not be reported in the Transportation row, but rather in the Administration and General row along with other administrative employee wages.

- — Row 009: Utilities: Expenditures for items such as gas, electricity, fuel, and water necessary for the operation of the provider entity's facility.

- — Row 010: Office Supplies & Materials: Expenditures for consumable office supplies such as:

- Office supplies and expenses

- Postage/Freight/Messenger service

- Copying/Printing

- Pencils/pens, folders, note pads, and the printing of office forms, letterhead, and envelopes

- — Row 011: Insurance: In this category, report insurance policy costs including building, professional and general liability, fire and theft, burglary, plate glass, automobile, etc. Credit this line with any dividends, refunds, and rebates received from insurance carriers or agents. Payments for employees' benefits, such as workers' compensation, unemployment, health, and disability relating to employees' benefits are only included if paid directly by the agency. Payments related to employee benefits made by insurance companies should not be entered on this line.

- — Row 012: Administration & General: Administrative employee salary and benefit expenditures along with other administrative expenditures not already included in other general service cost center rows incurred for maintaining the daily operations of the provider entity. These include:

- Program Administration Worker salary/compensation costs

- Program Administration Worker fringe benefits and payroll taxes:

- FICA taxes (Social Security and Medicare)

- Insurance (Life/Health)

- Pension & retirement

- Workers' compensation UID/disability

- Vacation accrual

- Metropolitan Commuter Transportation Mobility Tax (MCTMT), also known as the "MTA Tax"

- Certain State and Local Taxes, including:

- School/Property/Real Estate Taxes (applicable to NFP tax exempt agencies only)

- Sewer/Water taxes

- NYS corporation/franchise tax

- Electronic data processing (EDP)/computer expenses

- Telephone expenses

- Professional fees (e.g., accounting services, legal services, maintenance services, cleaning, bookkeeping, administrative computer services, and other administrative-related contracted purchased services not related to direct patient care)

- Training/Education/Recruitment

- Books/Dues/Subscriptions

- Interest

- Insurance

- Billing services

- Medicaid processing & collections services

- Payroll processing services

- Costs of advertising, public relations, or promotion (when such costs are specifically related to the provision of personal care services and are not for the purpose of attracting patients)

- Franchise/royalty fees

- — Row 013: Physicals/Uniforms/Immunizations: Expenditures for all employees (Direct Care and Administrative) for physicals, uniforms, and immunizations.

- — Row 014: Medical Supplies: Include any medical supplies such as masks, gloves, syringes, needles, medical monitors, and first aid equipment that is used by Direct Care workers to provide care to patients.

- Important notes:

- — The Grand Total row of Column 005 (Program Administration) on Schedule 3 should equal the Grand Total row of Column 001 (Program Administration) on Schedule 4. The Program Administration budgeted costs are the same on Schedules 3 and 4 but are allocated in different ways. On Schedule 4, Program Administration costs are reported in their appropriate General Service Cost Center rows.

- — If any professional staff will split their time between administrative and direct care services, their personnel expenses (e.g., salary, benefit, and payroll tax expenses) should be allocated across the Program Administration and Direct Care columns based on the time worked performing each type of service. However, only the program administration portion of their salary should be reported on Schedule 4, within the Program Administration column. The direct care portion of the personnel expenses should not be reported on Schedule 4 and should only be reported in Schedule 3.

- Column 002: Direct Care Non-personnel Costs - All non-personnel direct care budgeted costs should be reported within Column 002. No direct care worker wage, benefit, or payroll tax expenses should be reported on Schedule 4 (e.g., personal care aide salary expense). No costs are allowed to be reported in the cells with a gray background. Non-personnel direct care costs should be reported in the Medical Supplies row (Row 014).

Note: For the line items in Schedule 4b, please reference the Schedule 4, Column 001 guidance for details regarding appropriate inclusion of all budgeted costs. All items in this section deal largely with non-personnel expenses. Please note that these budgeted costs should be reported as budgeted costs for each general service cost center and should not be allocated throughout the cost centers.

Schedule 5b: Service Statistics

E Note: Schedules 5b require entity-level information.

Schedule 5b includes the expected service statistics broken down by service type and payor source at the entity level. Note that an agency is required to complete more than one of the following schedules if they expect to operate more than one of these entity types:

- Schedule 5b (for budgeted LHCSA service statistics) - A separate Schedule 5b table should be completed for each unique LHCSA entity.

Schedule 5b is used to aggregate units of service by program type for all individual entities operated by the agency as related to LHCSAs by reporting period. Agencies should report all anticipated visits/hours on Schedule 5 within the appropriate payor source column and service type row.

Please follow the below instructions while completing Schedule 5b:

- — While supporting documentation is not required to be provided for the Budgeted Projections Statement, it will be required in future years when the agency submits the completed Home Care Cost Report. All supporting documentation will be uploaded to the Secure File Transfer Protocol (SFTP) site at the following link: https://kmft.us.kpmg.com/.

- — For your Budgeted Projections Statement submission, the statistics are expected to be estimated as you have either not begun operations or have been in operation for less than a year. Examples of source documentation that agencies may be used to prepare the Budgeted Projections Statement Schedule 5 include:

- Budgeted Statistical data showing that anticipated number of patients, visits, and hours expected as well as anticipated payor source and service type

- Statistical report showing patient count, visit, hour, payor, and service type data for portion of year Agency has been in operations (if available)

- — Each entity table is broken down into two sections: reimbursable services and non- reimbursable services. The "Subtotal (reimbursable services)" row will calculate the total of the reimbursable service type statistics only. The "Grand Total" row will calculate the sum of the reimbursable and nonreimbursable service type statistics.

- The service type rows in which statistics are reported on Schedule 5 should match the service type rows for which costs were reported on Schedule 3.

- Service statistics related to nonreimbursable services should be reported in the "Other nonreimbursable services" row 010.

- Non-reimbursable service statistics should be recorded as positive values. The total reimbursable plus nonreimbursable service statistics should add up to the agency's grand total service statistics.

- — A description of the data that should be entered in each column of, 5b is included below:

- Columns 001, 004, 013, 016, and 019: Patients - Data entered into these columns should represent the budgeted number of patients expected to be served during the report period and data should be separated into the applicable columns based on expected reimbursement/payor sources (Medicaid Fee-for-Service [FFS], Medicaid Managed Care [MC], Medicare, Private Pay, or Other). Note the following:

- You should use the primary payor to determine where to report a patient (e.g., Medicaid versus Medicare for a dual-eligible patient).

- Note that the "Other" column should include commercial, government (such as Veterans Affairs and New York State Office for the Aging), workers' compensation, and no-fault insurance items. If any other items are included, agencies may be required to provide an explanation.

- Columns 002, 005, 014, 017, and 020: Visits/Days - Data entered in these columns should represent the total budgeted number of visits or days of service expected to be provided during the report period, associated with their given column header (Medicaid Fee-for-Service [FFS], Medicaid Managed Care [MC], Medicare, Private Pay, or Other). Note the following:

- You should use the primary payor to determine where to report the applicable visits/days (e.g., Medicaid versus Medicare for a dual-eligible patient).

- Note that the "Other" column should include commercial, government (such as Veterans Affairs and New York State Office for the Aging), workers' compensation, and no-fault insurance items. If any other items are included, agencies may be required to provide an explanation.

- Columns 003, 006, 012, 018, and 021: Hours - Data entered in these columns should represent the total budgeted number of hours for each service expected to be provided during the report period, associated with their given column header (Medicaid Fee-for-Service [FFS], Medicaid Managed Care [MC], Medicare, Private Pay, or Other). Note the following:

- You should use the primary payor to determine where to report the applicable hours (e.g., Medicaid versus Medicare for a dual-eligible patient).

- Note that the "Other" column should include commercial, government (such as Veterans Affairs and New York State Office for the Aging), workers' compensation, and no-fault insurance items. If any other items are included, agencies may be required to provide an explanation.

- Columns 010, 011, and 012: Dual-Eligible - If the agency provides services to patients who are considered "Dual-eligible," those service statistics must be reported in Schedule 5b in Columns 010 (patients), 011 (visits/days), and 012 (hours). If a patient is considered "dual-eligible," that means the patient has both Medicaid and Medicare coverage and as such, their service statistics must also be entered in either the Medicaid Columns 001 - 006 or the Medicare Columns 013, 014, and 015. The agency may not report the service statistics for the same patient and service type in both the Medicaid and Medicare columns. Instead, the agency should enter the service statistics in one or the other based on the anticipated primary payor. The service statistics should be reported in the Dual-eligible Columns 010, 011, and 012 AND within the Medicaid columns OR the Medicaid columns. That is because service statistics entered into the Dual-eligible columns are NOT counted in the Total Columns 022, 023, or 024. Only service statistics entered into the Medicaid, Medicare, Private Pay, and Other columns are included in the Total. As such, service statistics entered into the Dual-eligible columns that are not reported in any other column, will not be counted in the Totals.

- Column 007: Total Medicaid Patients - Column 007 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 001 (Medicaid Fee-for-Service Patients) and Column 004 (Medicaid Managed Care Patients).

- Column 008: Total Medicaid Visits/Days - Column 008 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 002 (Medicaid Fee-for-Service Visits/Days) and Column 005 (Medicaid Managed Care Visits/Days).

- Column 009: Total Medicaid Hours - Column 009 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 003 (Medicaid Fee-for-Service Hours) and Column 006 (Medicaid Managed Care Hours).

- Columns 022: Total Unique Patients - Column 022 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 001 (Medicaid Fee-for-Service Patients), Column 004 (Medicaid Managed Care Patients), Column 013 (Medicare Patients), Column 016 (Private Pay Patients), and Column 019 (Other Patients). Note that this column does not include the number of dual-eligible patients in the calculation. As such, Column 022 represents the total number of unique patients.

- Column 023: Total Unique Visits/Days - Column 023 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 002 (Medicaid Fee-for-Service Visits/Days), Column 005 (Medicaid Managed Care Visits/Days), Column 014 (Medicare Visits/Days), Column 017 (Private Pay Visits/Days), and Column 020 (Other Visits/Days). Note that this column does not include the number of dual-eligible visits/days in the calculation. As such, Column 023 represents the total number of unique visits/days.

- Column 024: Total Unique Hours - Column 024 does not require any information to be entered. This column is an automated calculation and reflects the sum of Column 003 (Medicaid Fee-for-Service Hours), Column 006 (Medicaid Managed Care Hours), Column 015 (Medicare Hours), Column 018 (Private Pay Hours), and Column 021 (Other Hours). Note that this column does not include the number of dual-eligible hours in the calculation. As such, Column 024 represents the total number of unique hours.

- Column 025: Total Entity Costs (from Schedule 3b, Column 001) This column does not require any information to be entered. This column will automatically populate the budgeted costs from Schedule 3, Column 001 for each entity and service type. This information will be used for the "cost per unit" calculation in Column 026 described below.

- Column 026: Total cost per unit (not reimbursement rate) -This column does not require any information to be entered. This column is an automated calculation and reflects the budgeted cost per unit of service based on budgeted data entered in Schedule 3 and Schedule 5. The cost per unit is NOT your budgeted Medicaid reimbursement rate. Instead, this column is meant to serve as a helpful check for providers to see if they reported their data accurately and consistently between Schedules 3 and 5. The cost per unit formula is included below for reference:

- Formula: Total Entity Costs from Column 025 on Schedule 5 / Total Units of service from Column 023 or 024 of Schedule 5 (hours or visits/days depending on the service type row)

- Column 027: Total cost per unit-Prior Year (not reimbursement rate) -This column does not require any information to be entered. This column is an automated calculation and reflects the cost per unit of service based on data entered in Schedule 3 and Schedule 5 from the prior year (i.e., the amount calculated in column 026 of the prior year's report). The cost per unit is NOT your budgeted Medicaid reimbursement rate.

- Column 028: Year-over-Year (YOY) Change -This column does not require any information to be entered. This column is an automated calculation and reflects the YOY change on the cost per unit from the current year and prior year.

- Report Fields - There are some fields in Schedule 5b that are not applicable to all agencies completing the projections statement. For example, certain service types, measure ‘units of service' in hours, not the number of visits, and vice versa. As such, all service type rows are aligned to their appropriate a ‘unit of service column' and allow for data entry. Cells that are grayed out do not allow for data entry because the service type row does not correspond to the ‘unit of service column' according to DOH.

Schedule 7b: Current Charge to the General Public

E Note: Schedule 7b requires entity-level information.

Schedule 7b includes the current charge to the general public. Note that an agency is required to complete more than one of the following schedules if they expect to operate more than one of these entity types:

- Schedule 7b (for budgeted LHCSA Current Charge to the General Public) - A separate Schedule 7b table should be completed for each unique LHCSA entity.

Please follow the below instructions while completing Schedule 7b:

- — While supporting documentation is not required to be provided for the Budgeted Projections Statement, it will be required in future years when the agency submits the completed Home Care Cost Report. All supporting documentation will be uploaded to the Secure File Transfer Protocol (SFTP) site at the following link: https://kmft.us.kpmg.com/.

- — Examples of source documentation that agencies may be used to prepare the Budgeted Projections Statement Schedule 7 include:

- Chargemaster

- Proposed Fee Schedule

- — A description of the data that should be entered in each column of Schedule 7b is included below:

- Column 001: Current Charge to the General Public - For each service that your entity expects to provide to private-pay patients, enter the anticipated public charge for each service type. These charges are what an individual with no coverage would pay for a service and should reflect the charge per unit of service (i.e., visit, hours, days).

- For any information entered in the "Other" line, an explanation may be required to indicate what service this amount relates to.

Note that the service type rows that have public charge reported on Schedule 7 should match to the service type rows with budgeted statistics reported on Schedule 5, unless private-pay patients will not be serviced for that service type.

Appendix A - Personal Care Rate Codes

| Personal Care | Rate Codes DOH Uses | |

|---|---|---|

| LEVEL I | 2601 | LEVEL I, ONE CLIENT HOURLY - No Reduction |

| 2602 | LEVEL I, 2 CLIENTS HOURLY - 2601/2 | |

| 2593 | LEVEL I, ONE CLIENT, QUARTER HOUR - 2601/4 | |

| 2594 | LEVEL I, 2 CLIENTS, QUARTER HOUR - 2602/4 | |

| LEVEL II | 2622 | LEVEL II, ONE CLIENT HOURLY - No Reduction |

| 2623 | LEVEL II, 2 CLIENTS HOURLY - 2622/2 | |

| 2595 | LEVEL II, ONE CLIENT, QUARTER HOUR - 2622/4 | |

| 2596 | LEVEL II, 2 CLIENTS, QUARTER HOUR - 2623/4 | |

| HARD TO SERVE | 2626 | LEVEL II, HARD TO SERVE, ONE CLIENT - No Reduction |

| 2627 | LEVEL II, HARD TO SERVE, TWO CLIENTS - 2626/2 | |

| 2597 | 1 CLIENT, HARD TO SERVE, QUARTER HR - 2626/4 | |

| 2598 | 2 CLIENTS, HARD TO SERVE, QUARTER HR - 2627/4 | |

| SHARED AIDE | 2501 | SHARED AIDE LEVEL I, HOURLY - No Reduction |

| 2502 | SHARED AIDE LEVEL II, HOURLY - No Reduction | |

| 2507 | SHARED AIDE LEVEL I, QUARTER HOUR - 2501/4 | |

| 2508 | SHARED AIDE LEVEL II, QUARTER HOUR - 2502/4 | |

| LIVE-IN | 2632 | LIVE-IN, ONE CLIENT - No Reduction |

| 2633 | LIVE-IN, TWO OR MORE CLIENTS - 2632/2 | |

| NURSING VISITS | 2742 | NURSING SUPERVISION - No Reduction |

| 2787 | NURSING ASSESSMENT - No Reduction |

Appendix B - Schedules 3 and 4 Categorization of Costs

For additional guidance on Schedule 3 and 4 categorization of costs, please refer to the Home Care Cost Report Instructions within the "Instructions" tab of the web-based Tool, and on the DOH website here: Home Care Cost Report Resources.